Irs Useful Life Of Carpet

Http Www Irs Gov Pub Irs Prior I4562 1991 Pdf

We Do Water Extracting Carpet Dry Cleaning And Carpet Restoration In Frederick Md Iicrc Certified Professionals In Frederick Carpet Care New Gadgets Hamilton

Instructions For Form 5471 02 2020 Internal Revenue Service

How To Maximize Your Real Estate Depreciation

Income Tax Exemption Vs Tax Deduction Vs Tax Rebate Vs Tds Key Differences Income Tax Tax Deductions Tax Exemption

Form W 2 What You Need To Know Tax Forms W2 Forms Irs Forms

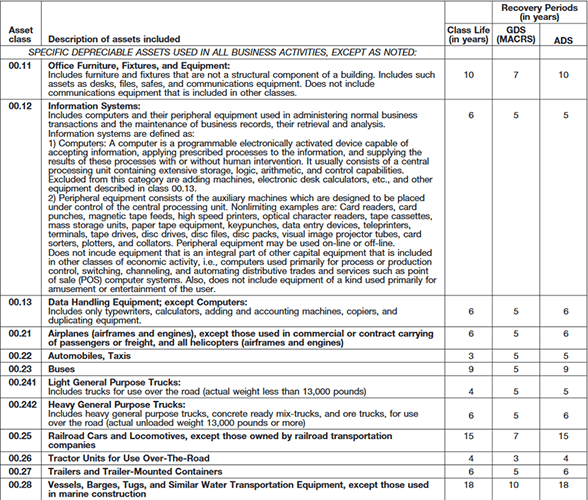

Instead you generally must depreciate such property.

Irs useful life of carpet.

Mermaid 71 X 34 Freestanding Soaking Bathtub Soaking Bathtubs Wyndham Collection Kitchen Installation

Ancestry Login Fillable Family Tree Fill Online Printable Fillable Blank Pdffiller In 2020 Irs Forms Tax Forms Fillable Forms

C2c Tutorial Corner To Corner Crochet By Redagape Blog C2c Manta De Ganchillo Mantas De Ganchillo Puntadas De Ganchillo

Learning Organized Home Maintenance Binder With Repairs And Maintenance I Would Add In Pa Home Maintenance Repair And Maintenance Best Bathroom Paint Colors

Facing A Flood Is Something That No Family Wants To Go Through But Unfortunately Sometimes Life Surpr Water Damage Repair Flood Insurance How To Clean Carpet

28 Form W 2 Fillable In 2020 Classroom Newsletter Template Class Newsletter Template Obituaries Template

How Long Should I Keep It For Free Printable Paper Organization Organizing Paperwork Organization Hacks

Https Homelinemn Org Wp Content Uploads Babler V Penn No 62 Cv 13 1539 Pdf

Writing A Irs Penalty Abatement Request Letter With Sample Resignation Letters Tax Return Writing

The Shedtek Professional Pet Hair Removal Tool Is The Best Product For Removing Dog And Cat Hair From Car Interio Cleaning Pet Hair Pet Hair Removal Clean Sofa

Infographic Hospitality In The Vacation Rental Industry Vacation Rental Infographic Hospitality

Find The Right Low Interest Credit Card Flowchart Nerdwallet Low Interest Credit Cards Best Credit Card Offers Credit Card Deals

What Does Depreciation Mean Ionos

Matted Political Cartoon By John Trever Irs Audit 8in X 10n 25 Political Cartoon Weemsgallery Com Art Pages Political Cartoons Wall Art

Accounting For Non Accountants 3e Pdf Learn Accounting Learn Business Accounting

Holiday Cookie Gift Basket The Tomkat Studio Blog Cookie Gift Baskets Baking Gift Basket Holiday Cookie Gift

Helpful Student Tips For That A Estate Planning Attorney Student Estate Planning

How To Get Mildew Smell Out Of Car Mildew Smell Clean Car Carpet Carpet Cleaning Hacks

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctnliasrclwhpao7wftwjruskhb6v7vegwfzodeuius7aqplvdv Usqp Cau

Forbo Marmoleum Modular T3216 Moraine Sold In Cartons 26 91 Sq Ft Ctn Size 10 X 10 By Idecor Flooring Materials Linoleum Flooring Ceramic Floor Tile

Cat Food Chart From Catinfo Org Food Charts Cat Food Cat Diet

The 46 Most Brilliant Life Hacks Every Human Being Needs To Make Life Easier Useful Life Hacks Life Hacks Weekly Workout Plans

8 Home Hazards And How To Mitigate Them Water Damage Repair Flood Insurance How To Clean Carpet

23 Things You Need If You Ve Basically Never Cleaned Your Home Correctly In 2020 Cleaning Broom And Dustpan Natural House Cleaning

Source : pinterest.com