Interest Rate Cap Floor Straddle

:max_bytes(150000):strip_icc()/understandingstraddles2-c0215924b5ba43189e1a136abc5484bf.png)

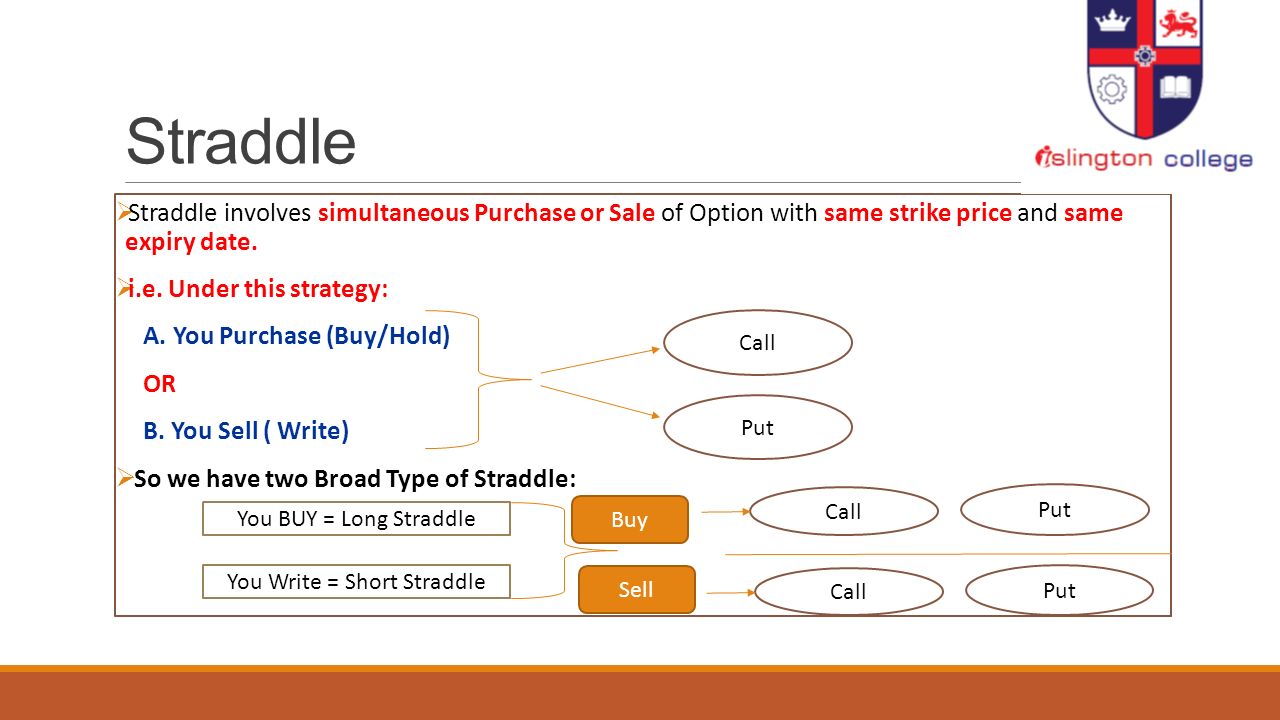

Straddle Definition

Trading Strategies Involving Options Analystprep Frm Part 1

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

10 Options Strategies To Know Put Option Interactive Brokers Writing Strategies

7 Popular Options Trading Strategies Magnifymoney

Long Call Ladder Explained Online Option Trading Guide

An example of a cap would be an agreement to receive a payment for each month the libor rate exceeds 2 5.

Interest rate cap floor straddle.

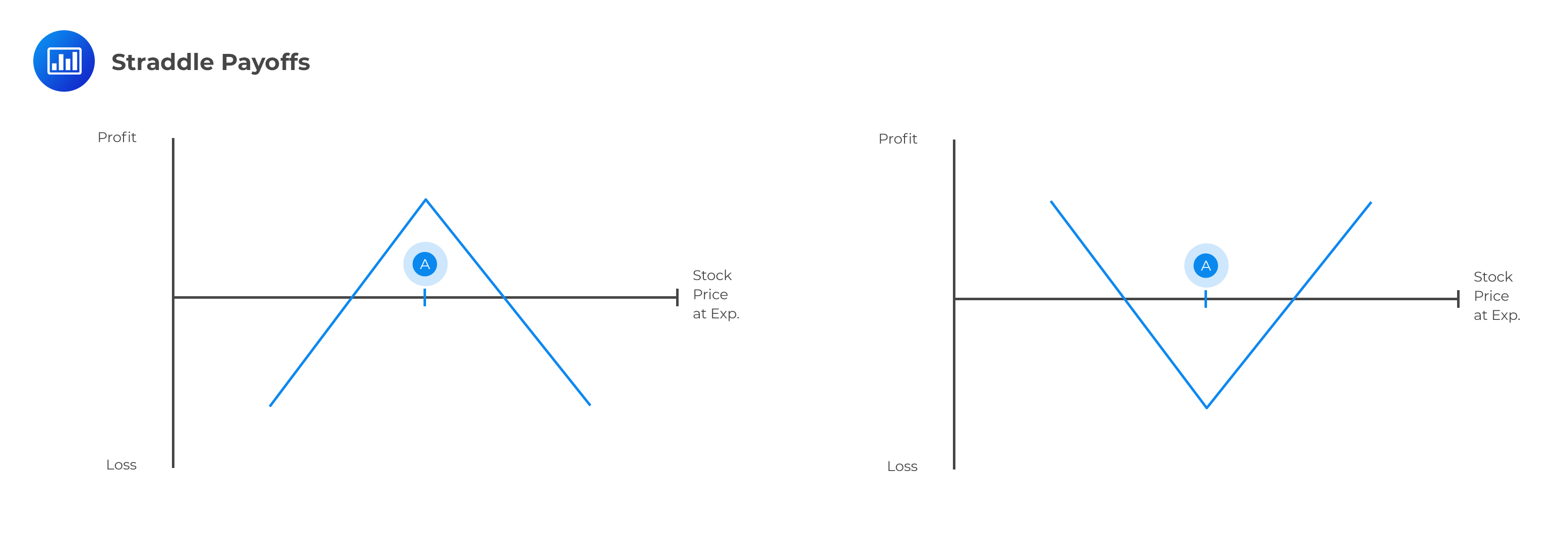

Long Straddle Definition Day Trading Terminology Warrior Trading

/10OptionsStrategiesToKnow-02_2-8c2ed26c672f48daaea4185edd149332.png)

Protective Put Definition

Managing Risk Via The Financial Markets In The Uk Financial System Fifth Edition

Installation Instructions Installation Instruction Installation Instructions

:max_bytes(150000):strip_icc()/dotdash_Final_Seagull_Option_Apr_2020-01-ddc8d06ec2ee477d95c15ea16722887d.jpg)

Seagull Option Definition

How To Do Straddle Split Workout Challange Flexibility Workout Yoga Body

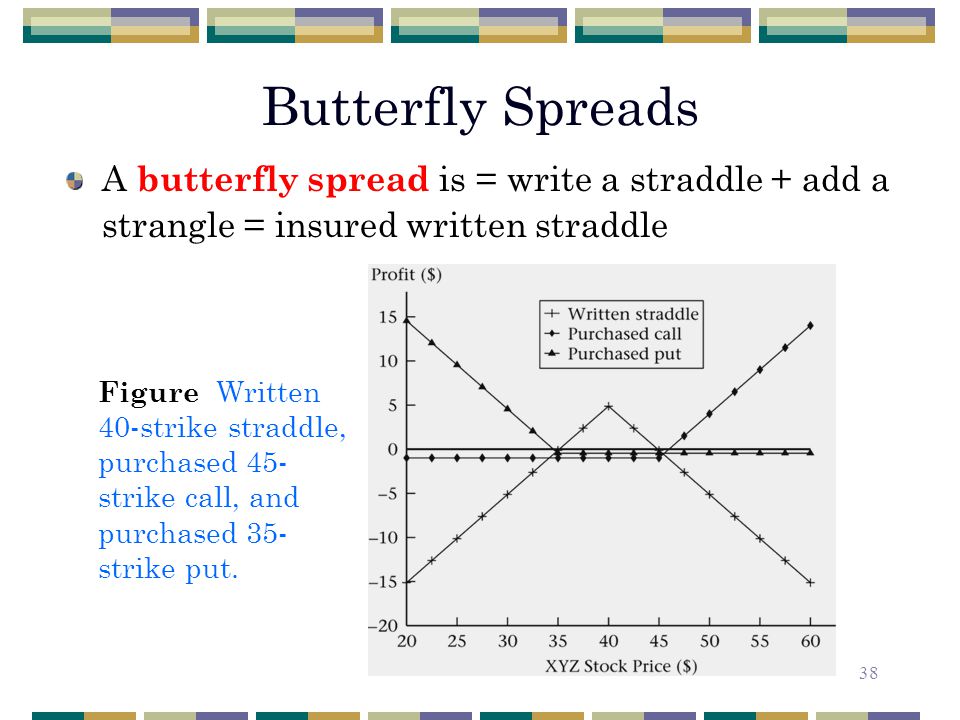

Chapter 3 Insurance Collars And Other Strategies Ppt Video Online Download

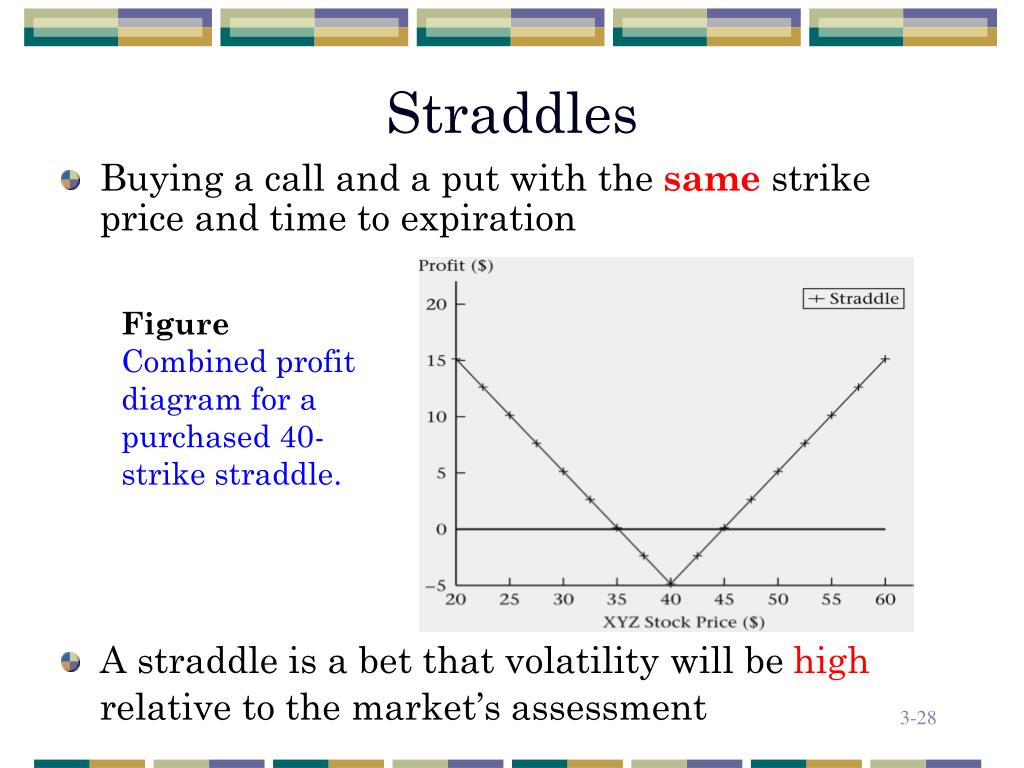

Fintech Chapter 12 Options Ppt Download

Top 9 Agility Ladder Drills A 30 Minute Speed Ladder Routine To Try In 2020 Agility Ladder Agility Ladder Drills Ladder Workout

Insurance Collars And Other Strategies Ppt Download

Https Link Springer Com Content Pdf 10 1007 2f978 1 349 13586 8 17 Pdf

Https Www Isda Org A Ocide Isda Structures Survey Final Results Pdf

Image Result For Funds Fees Bloomberg Chart Financial Charts Investing Strategy Chart

Newsletter Thoughts Archives Party At The Moontower

Ppt Faculty Of Business And Economics University Of Hong Kong Dr Huiyan Qiu Powerpoint Presentation Id 3531486

Introduction To Financial Engineering Aashish Dhakal Week 5 Options Plain Vanilla Exotics Strategies Ppt Download

2 The Volatility Cube New York University Pages 1 16 Text Version Fliphtml5

Irs Form 6781 Download Fillable Pdf Or Fill Online Gains And Losses From Section 1256 Contracts And Straddles 2019 Templateroller

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqyuwncx1nhvc7prgswec2zywuyfmvxndz2kce K0bqmxysrrpk Usqp Cau

Chapter 3 Insurance Collars And Other Strategies Ppt Download

Pin On Resolute Fitness

The Challenges Facing Home Depot Realmoney

Https Www Finance Senate Gov Imo Media Doc Jct 20memo 20on 20moda 202017 Pdf

Https Www Tandfonline Com Doi Pdf 10 1080 10803548 2020 1733343 Needaccess True

Source : pinterest.com